Health Insurance Brokers Guide to No Claims Discounts

- greg webster

- Jun 2

- 5 min read

Understanding PMI No Claims Discount Benefits

Navigating the world of private medical insurance (PMI) can often feel like a labyrinth of jargon and fine print. Among these complexities, the No Claims Discount (NCD) is a critical aspect that can significantly impact both your premiums and your policy's value. But what does NCD mean in the context of private medical insurance, and how does it work? Here, we break down this concept in simple terms to help you unlock the potential benefits of your PMI policy.

A No Claims Discount is essentially a reward for policyholders who do not make any claims on their insurance within a specific period. This benefit stems from the insurance provider's desire to incentivize healthy individuals or those who may not require medical attention frequently. If you maintain a claim-free history, insurers often reward you with lower premiums when it comes time to renew your policy.

What is a no claims discount? Explained by a health insurance broker

A no claims discount (NCD) is a percentage reduction applied to the base cost of your private health insurance. The longer you go without making a claim, the higher the discount you retain. Make a claim, and that discount can drop, sometimes significantly.

It sounds simple enough, but PMI NCDs work quite differently to the no claims discounts most people are familiar with from car insurance.

How is a PMI no claims discount different from a car insurance NCD?

With car insurance, you start from zero and build your discount up over time. It feels like a reward for good driving.

Private medical insurance works almost in reverse. Most insurers start you at a high discount, often around 70% off the base premium, from day one.

In practical terms, this means that making a claim in the early years of a PMI policy can have a substantial impact on your renewal premium, because you're falling from a high starting point.

The Benefits of No Claims Discounts

Understanding PMI No Claims Discount benefits can empower you as a policyholder. Here are some advantages to keep in mind:

Lower Premiums: Enjoy reduced monthly costs, allowing you to allocate budget elsewhere.

Encouragement for Healthy Lifestyle: The desire to maintain a claim-free record often motivates individuals to engage in healthier practices.

Transferable Discounts: If you switch providers, you may bring your NCD along, keeping your benefits intact.

However, also be aware that if a claim is made, you may lose your discount status, which can impact your future premiums. Therefore, it’s critical to weigh the decision carefully before filing claims for minor issues that could be managed otherwise.

How do NCD scales work?

Most PMI providers use a sliding scale, typically up to level 14. You start near the top, and:

If you make no claim in a policy year, you usually move up one level, slightly increasing your discount

If you make a claim, you can drop several levels at once, depending on the size of the claim and your insurer's specific rules

The further down the scale you fall, the larger the percentage gap between each level tends to be. In other words, the penalty for claiming gets more expensive the more you claim.

Do all PMI providers offer an NCD?

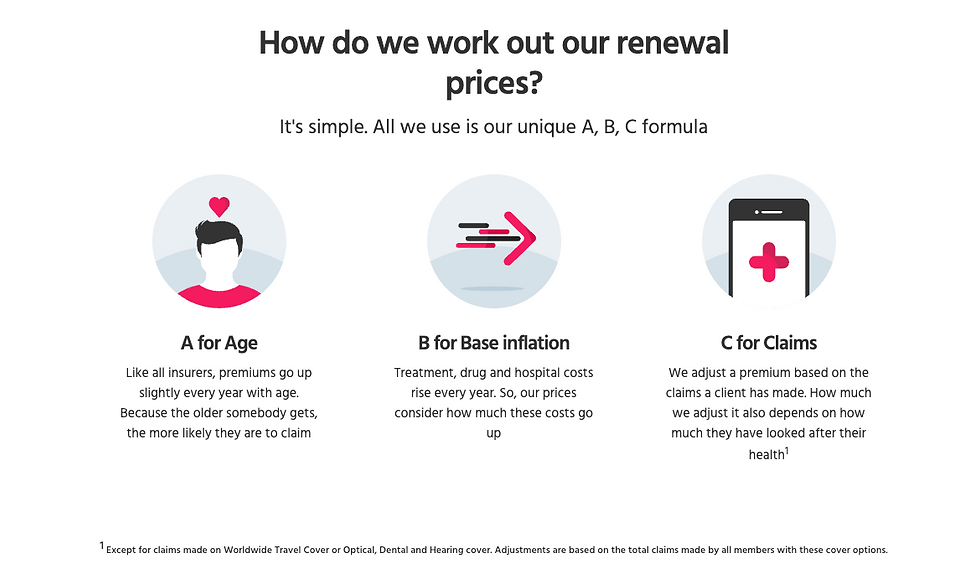

No. Some providers, including Vitality and Freedom Health Insurance, do not use a traditional NCD sliding scale. Vitality uses its own pricing model (image below), though your claims history still influences your renewal. Freedom Health Insurance doesn't offer an NCD at all, though again, claims are still likely to factor into your price at renewal.

If NCD protection matters to you, it's worth checking the specific model used by any provider you're considering.

How do different providers compare?

The major providers that do offer an NCD including Aviva, AXA Health, Bupa, The Exeter, WPA each have their own starting levels, discount percentages, and rules around how claims affect your position on the scale.

One of the most meaningful differences is how providers treat smaller claims. Some won't move you down the scale at all for claims below a certain threshold. Others will penalise any claim, regardless of size.

For example, a claim below £300 might have no effect on your NCD with one insurer, while triggering an immediate drop of three levels with another. Over time, that difference can be substantial.

Can you protect your no claims discount?

Some providers offer NCD protection as an optional add-on. This means that if you make a claim, your discount level is preserved, though you'll usually lose the protection itself for one or two years after claiming, and will need to go claim-free to reinstate it.

Aviva, AXA Health, and The Exeter are among the providers that currently offer this option. It's worth weighing up the additional cost against the potential premium impact of losing discount levels.

Does your excess affect your NCD?

Yes, and this is something that's often overlooked. Your excess is the amount you agree to contribute towards any claim before your insurer pays out. Crucially, if the cost of your treatment falls below your excess, your insurer doesn't pay anything, and your NCD isn't affected.

A higher excess therefore acts as a natural NCD buffer for smaller claims. It also reduces your monthly premium. The trade-off is that you pay more out of pocket if you do need treatment, so the right excess level depends on your circumstances and how likely you are to claim.

In some situations, particularly for minor treatments, it may even be worth paying for treatment yourself to avoid triggering a drop in your NCD.

What types of claims don't affect your NCD?

Not all claims move you down the scale. The specifics vary by provider, so it's always worth checking your policy documents or speaking to your adviser if you're unsure whether a particular type of claim will affect your discount.

The key things to remember about PMI no claims discounts

PMI NCDs can feel complex, but the core principles are straightforward:

You start with a high discount and have more to lose than to gain

Claiming, especially for larger amounts, can significantly increase your renewal premium

Different providers treat small claims very differently

Your base premium, not just the discount percentage, determines the real financial impact

Your excess can protect your NCD for smaller claims

NCD protection is available with some providers and worth considering

If you're unsure how your current NCD works, or whether you're on the right policy for the way you use your cover, we're happy to help. Speaking to an adviser before you claim, or before you renew, can make a real difference to what you pay.

This article is for information purposes only and does not constitute financial advice. Please speak to one of our health insurance brokers for a recommendation tailored to your circumstances.

Frequently Asked Questions

What happens if I make a claim under my insurance policy?

If you make a claim, your No Claims Discount level may decrease, which can lead to higher premiums during your next renewal.

How can I find out my current No Claims Discount status?

You can typically check your No Claims Discount level on your insurance provider's portal policy certificate.

In a world where healthcare waits are often long and frustrating, private medical insurance offers the peace of mind that can drastically improve your quality of life. Understanding and leveraging the No Claims Discount can ensure you’re not only receiving top-notch care when needed but also taking full advantage of your investment. For further insights into the intricacies of private health insurance, check out our guide on Why Renewals Are the Most Important Part of Your Private Health Insurance Policyor explore The Ultimate Guide to Private Health Insurance in the UK for broader information.

Comments